Could COVID-19 pandemic create a ‘perfect storm’ for wholesale electricity prices?

In part one of this two-part series RepuTex discuss their medium-term expectations for the National Electricity Market (NEM), specifically the impact of COVID-19 on forecast wholesale prices in line with their latest Australian Electricity Outlook (AEO).

Part two of the series will discuss their longer-term expectations for price formation under their Alternative Case, reflecting AEMO’s “Step Change” shift to renewable energy in line with a “well below 2°C” Paris climate commitment (e.g. achieving net-zero emissions prior to 2050).

Background to Australian Electricity Outlook (AEO)

RepuTex’s quarterly AEO provides an outlook for wholesale electricity prices for each region of the NEM over medium- (16 quarters) and long-term horizons (annually to 2040); an outlook for Large-scale Generation Certificates (LGC) prices to 2030; forecast market outcomes such as change in capacity and generation mix; and analysis of the major factors impacting the electricity market in the forecast period.

Modelling considers a Central Case for electricity price development in line with RepuTex’s view of the current transition of the energy industry, along with an Alternative Case reflecting AEMO’s “Step Change” shift to renewable energy (discussed in part two of this series), accounting for faster technological improvements and more aggressive action on climate change in line with a “well below 2°C” Paris climate commitment (net-zero emissions prior to 2050).

Sensitivities are also considered as a complement to each scenario, helping to identify the magnitude of impact of key assumptions and understand pricing paths.

COVID-19 impacts on demand, gas prices and renewable energy commissioning

The coronavirus pandemic could help to create a perfect storm for the wholesale electricity market, with the potential for lower demand, lower gas prices and the commissioning of large renewable energy projects to depress electricity prices, depending on the extent and duration of lockdown restrictions.

At this point, the severity of lockdown restrictions is unknown, as is the timeframe for when restrictions will be eased and the time it will take to return to ‘normal’ demand for electricity. While it is too early to draw clear conclusions for demand, as we continue to move through the different stages of lockdown restrictions scenarios for reduced demand are of interest.

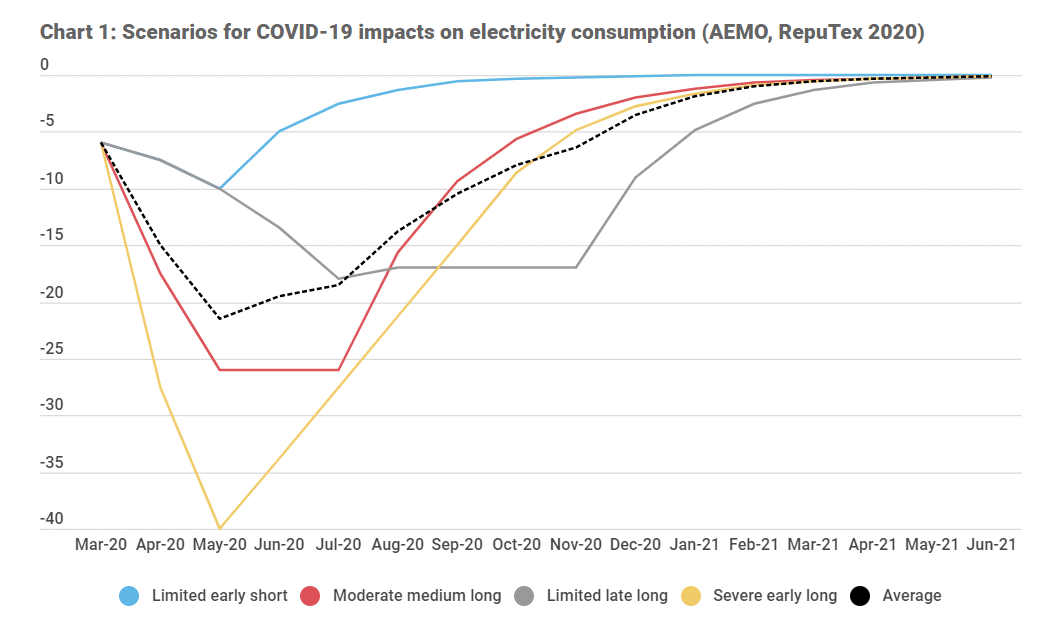

Given the short and medium-term uncertainty, we consider four scenarios for COVID-19 impacts on demand, adapted from AEMO’s Forecasting Reference Group, covering a reduction in electricity consumption from 10-40 per cent. This range reflects impacts from the current average for moderately restricted grids to more severe impacts such as those seen in Chinese provinces prior to the easing of lockdown restrictions. Scenarios reflect a possible quick ‘v-shaped’ rebound in consumption, or a sustained lockdown resulting in a ‘u-shaped’ rebound; with both substantially affecting electricity prices for financial year 2020-21 and a return to ‘normal’.

Chart 1: Scenarios for COVID-19 impacts on electricity consumption (AEMO, RepuTex 2020)

While electricity consumption volumes are not yet depicting a steep decline, scenarios assume a decline in demand over April and May 2020 as industrial facilities continue to close or reduce consumption, with restrictions eased by July 2020 and a return to ‘normal’ electricity consumption levels 12-months later.

Relative to the past five-year average, operational volumes (‘grid demand’) are down only 2 per cent this year, in line with recent trends, held up due to Australia’s reliance on industrial loads, such as coal mining, which have not yet been substantially impacted by COVID-19. While there is significant uncertainty around the extent of demand impacts, the AEMO scenarios are informative given the progressive enforcement of lockdown restrictions, and the potential for further industrial facility closures as positive on-site cases are recorded. A relatively sharp but temporary reduction in electricity demand over future months therefore remains plausible, and is of interest to consider.

In addition to lower forecast consumption, the last few weeks have seen a notable decline in oil demand (COVID-19 induced) coupled with increased production from OPEC countries. This has led to global oil prices decreasing to about half of their 2019 value, while holding domestic gas prices down. In turn this could see lower peak electricity prices and reduced impetus to open up new Australian gas basins.

On the supply side, around 1.6 GW of solar and wind capacity has been commissioned in FY19-20, leading to 27.5 TWh of solar and wind for the financial year-to-date, now just 0.6 TWh behind last year’s total solar and wind generation. Although we expect utility-scale solar and wind commissioning could hibernate for the next one to two quarters due to COVID-19 disruptions, we continue to forecast a total of 6.1 GW of solar and wind to be commissioned over the next two years, along with the contribution of another 1.2 GW of new rooftop Photovoltaics.

COVID-19 impacts may result in strong divergence in power price declines between regions

Combined, the confluence of potential COVID-19 demand cuts, lower domestic gas prices and the commissioning of large renewable energy projects could result in a strong divergence in power price declines between different regional markets, with prices forecast to potentially decline an average of 20 per cent in 2021 relative to a pre-COVID setting should lower demand scenarios transpire.

While we acknowledge the uncertainty attributed to the timing and scale of potential COVID-19 demand cuts, outcomes suggest the weighted average NEM wholesale price (weighted average of all regions) could average around $69 per megawatt-hour (/MWh) for 2019-20, declining toward $55/MWh over the next two years before recovering back above $60/MWh, slightly higher than current futures prices.

Despite lower prices under this scenario, we do not expect the medium-term environment to kill-off renewable energy investment, particularly at the largest-scale, with new mega-projects able to compete under $50/MWh, such as Acciona’s 1 GW MacIntyre Wind Farm, scheduled to be fully commissioned in 2024. Impacts are more likely to be felt at the lower end of the market, with smaller projects more adversely affected by negative factors such as the lower Australian dollar and associated higher supply chain costs, with the low wholesale electricity price environment modelled here to potentially disrupt the economics of these projects.

Request a demo

Or just email on

info@azility.co